The Austin and Central Texas residential real estate market has been one of the most watched economic landscapes in the country over the last few years. Following the historic highs of the pandemic-era boom, the market has undergone a significant multi-year recalibration.

Using data sourced from the Austin Board of REALTORS® (ABoR) MLS spanning from January 2022 through May 2026, we look into exactly how the market has shifted, comparing our latest numbers with previous years to see where the market is heading next.

1. Year-over-Year Snapshot: May Market Comparison

To understand where the market stands today, let’s look at the data from the latest available month (May 2026) and compare it directly to May of last year (2025), two years ago (2024), and the peak frenzy of four years ago (2022).

| Metric | May 2026 | May 2025 | May 2024 | May 2022 |

| Median Sales Price | $440,000 | $449,900 | $459,450 | $550,000 |

| Closed Sales | 2,953 | 3,021 | 2,968 | 3,633 |

| Sales Dollar Volume | $1.74B | $1.78B | $1.76B | $2.48B |

| Months of Inventory | 4.7 | 5.0 | 4.9 | 1.2 |

| New Listings | 4,786 | 5,716 | 5,243 | 5,231 |

| Active Listings | 12,508 | 14,673 | 12,211 | 4,173 |

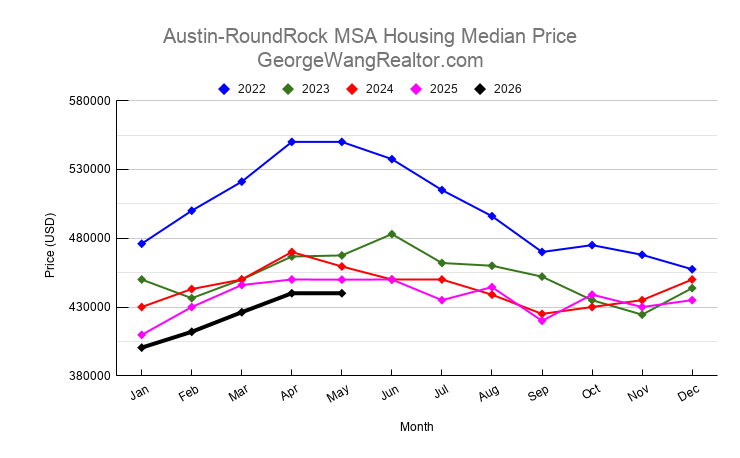

2. Median Sale Price: Finding a Sustainable Floor

The median sales price in Central Texas has carved out a clear path of stabilization following its dramatic peak in the spring of 2022.

- The Peak to Correction: In May 2022, the median sales price reached an staggering high of $550,000. As mortgage rates climbed throughout 2022 and 2023, prices felt downward pressure, sliding into the mid-to-high $400,000 range.

- The New Normal: Looking at the spring cycles of 2024, 2025, and 2026, the market has found a predictable seasonal rhythm, peaking each spring before tapering slightly in the fall. However, each subsequent peak has lowered slightly ($459k in May 2024, $449k in May 2025, and $440k in May 2026).

- The Takeaway: Prices are no longer in a freefall; instead, they are slowly discovering a sustainable, realistic floor that aligns more closely with local income levels and higher interest rate environments.

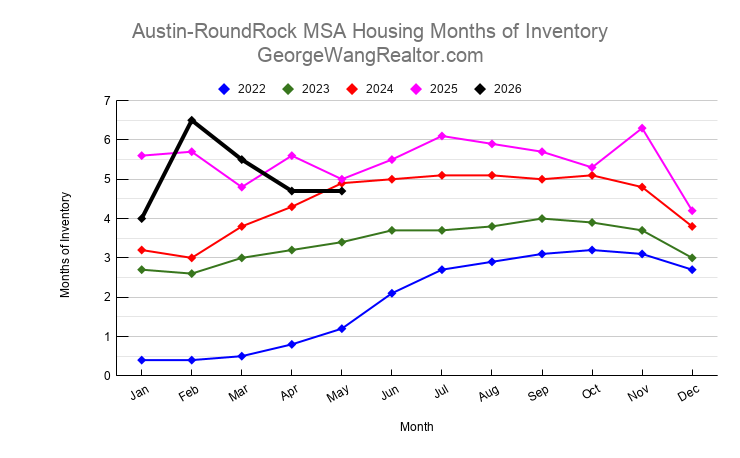

3. Months of Inventory: Shifting Power Back to Buyers

Months of inventory is the primary indicator of market balance. A 6-month supply is widely considered a healthy, balanced market between buyers and sellers.

- Severe Scarcity (2022): In early 2022, inventory sat at a microscopic 0.4 to 0.5 months. Sellers held absolute leverage, often resulting in fierce bidding wars.

- The Supply Surge (2024–2025): Supply expanded dramatically, peaking at 6.3 months in November 2025. This marked the first time in years that the local market crossed firmly into “buyer’s market” territory.

- Current Status: As of May 2026, inventory has compressed down slightly to 4.7 months. While this is down from the 2025 highs, it represents a highly functional, competitive, and accessible market for everyday buyers compared to the severe gridlock of 2022.

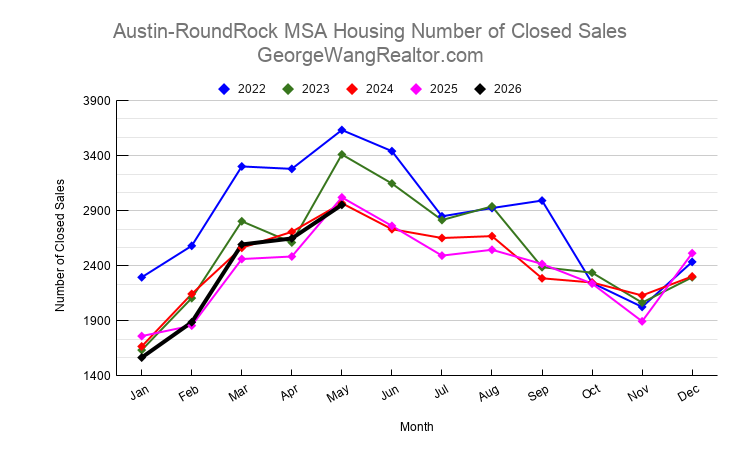

4. Closed Sales: Demand Stays Durable

Despite major shifts in pricing and financing costs, the pure volume of home sales has shown remarkable resilience.

- The Soft Landing: Closed sales naturally dropped from the hyper-inflated 2022 levels (which saw over 3,600 sales in May 2022) down to the mid-2,000s during seasonal lows.

- Consistent Baselines: Looking at May numbers across 2024 (2,968), 2025 (3,021), and 2026 (2,953), consumer transaction volume has essentially leveled out. People are still moving to and within Central Texas. The drop in prices has helped maintain transaction velocity, keeping sales volume healthy despite elevated borrowing costs.

5. New and Active Listings: Sellers Adjusting to Reality

Inventory levels are driven heavily by seller behavior, and the data shows a significant shift in how sellers are reacting to the market.

- Inventory Peak Check: Active listings reached a massive peak in the summer of 2025, hitting an all-time high of 17,662 homes on the market in June 2025. This oversupply was fueled by a huge spike in new listings that spring (climbing to 5,716 in May 2025).

- Seller Pullback in 2026: In May 2026, new listings dropped back down to 4,786 (a 16.3% decrease from May 2025). Sellers are becoming more strategic, recognizing that they can no longer list their properties at premium prices and expect an immediate handoff. This pullback in new entries has helped absorb the excess active inventory, bringing total active listings down to 12,508.

Conclusion

The Central Texas real estate market has officially graduated from its post-pandemic hangover and entered a phase of mature stabilization. The astronomical equity gains of 2022 have normalized into a market characterized by realistic home pricing, healthy inventory levels hovering just under 5 months, and a sustainable volume of closed sales. For sellers, pricing precision and property presentation are now non-negotiable pieces of a successful strategy. For buyers, the current environment offers a rare combination of choices, room for negotiation, and prices that have retreated roughly 20% from their historical peaks—making this the most approachable Central Texas housing market we’ve seen in half a decade.

If you have any questions or need any assistance in finding your new home or investment property, please contact me and I will be more than happy to work with you. You can read my client testimonials here.

Please also check out our rebate program which is a win-win situation for my buyer.